| The annual rate of UK inflation fell more sharply than expected, down to 2.8% in the year to April | Britain’s economy grew by 0.3% in March, defying expectations of a slight contraction linked to global conflict | According to ONS, the unemployment rate increased slightly to 5.0% in the three months to March |

Inflation eases, but Middle East conflict remains a concern

The annual rate of UK inflation fell more sharply than expected, dropping to 2.8% in the year to April from 3.3% in the year to March, according to the Office for National Statistics (ONS). Analysts had predicted a reading of around 3.0%.

ONS attributed the decline largely to lower household energy bills, reflecting a combination of government support measures and weaker wholesale energy prices in the period prior to the escalation of tensions in the Middle East. While this has helped ease cost pressures for now, the outlook remains uncertain and the improvement may prove temporary. Economists widely expect inflation to rise again in the coming months, with forecasts suggesting it could approach 4% by the end of the year. The ongoing conflict continues to drive volatility in global energy and food prices, which is likely to feed through to UK inflation. The Bank of England has warned that, under a more pessimistic scenario, inflation could reach as high as 6.2% early next year, marking a significant shift from earlier projections that had anticipated a return to the 2% target.

The Confederation of British Industry (CBI) warned that the latest inflation data ‘does not yet fully capture the inflationary impact of developments in the Middle East… As a result, inflation is likely to rise again in the months ahead, potentially peaking around the turn of the year.’

Fuel prices are already showing signs of strain, with petrol and diesel costs fluctuating in response to global uncertainty. In May, the government announced the extension of the 5p Fuel Duty cut until the end of the year, at an estimated cost of £455m. Meanwhile, discussions continue between the Treasury and major supermarkets regarding potential voluntary price caps on essential food items to help mitigate rising living costs.

Surprise UK growth fails to ease pressure on public finances

Britain’s economy grew by 0.3% in March, defying expectations of a slight contraction linked to disruption from the war. According to ONS, the increase was partly driven by consumers and businesses bringing forward spending ahead of anticipated price rises.

This stronger monthly performance contributed to first-quarter growth of 0.6%, marking the fastest pace in a year and the strongest among G7 nations to have reported figures so far. Car sales and leasing were among the standout areas, while retailers noted increased demand from motorists stocking up on fuel as petrol prices rose sharply. Both construction and retail sectors played a key role in the quarterly rebound.

Despite this positive momentum, the outlook remains uncertain. In the month, the International Monetary Fund (IMF) upgraded its forecast for UK growth this year but cautioned that the war, alongside ongoing ‘domestic uncertainty,’ could weigh on economic activity later in the year.

Chancellor Rachel Reeves welcomed the figures as evidence that the government has “the right economic plan.” She also warned that the Labour leadership contest risks destabilising the economy at a critical time. This concern has been reflected in financial markets, with government borrowing costs rising notably. Ten-year gilt yields briefly exceeded 5.17% in the month, their highest level since 2008, amid heightened political uncertainty. While borrowing costs have increased across Europe since the onset of the conflict, movements in the UK have been more pronounced.

Public sector borrowing rose to £24.3bn in April, an increase of £4.9bn compared with the same month last year and the highest April figure since the pandemic. Debt interest payments reached a record £10.3bn for the month, as higher benefit costs and State Pension increases pushed spending well above tax revenues.

Markets

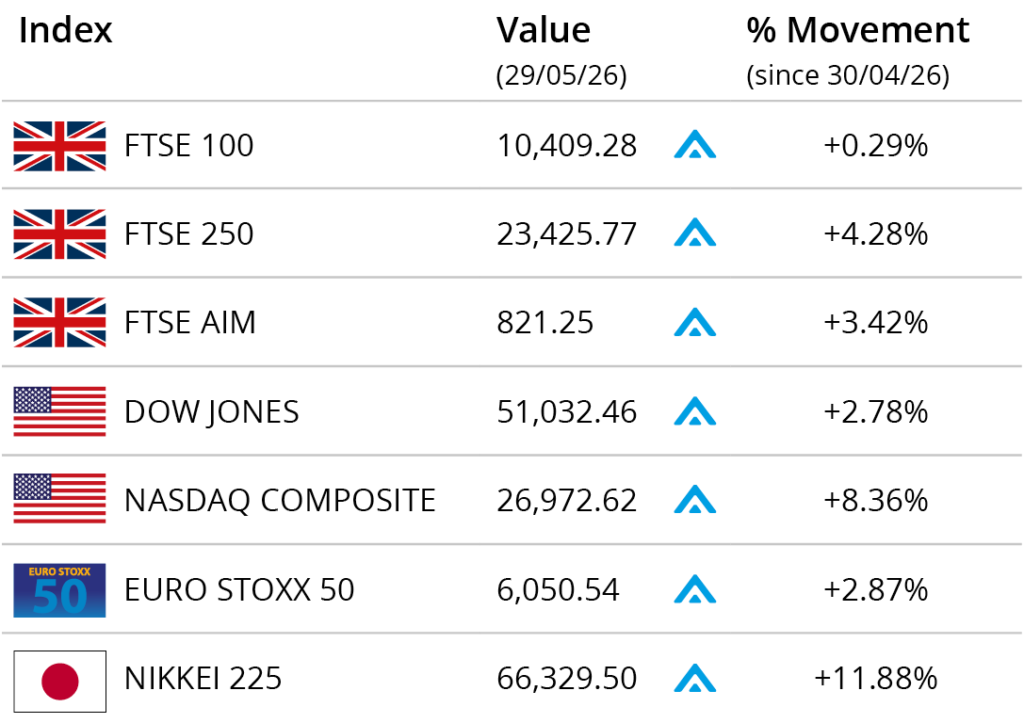

At the end of May, major global markets closed the month in positive territory. Wall Street’s main indexes hit record closing highs on the last trading day of the month, as investors awaited details of a potential US-Iran deal.

Investor sentiment was also buoyed by easing energy costs, robust earnings results and sustained enthusiasm around AI, with technology stocks leading the advance. In the US, the tech-focused NASDAQ recorded a monthly gain of over 8% to close on 26,972.62, while the Dow Jones closed the month up 2.78% on 51,032.46.

On home shores, the FTSE 100 closed the month up 0.29% on 10,409.28. At the end of May, London’s blue-chip index lacked confidence in the prospect of Trump agreeing a deal with Iran. Meanwhile, the FTSE 250 ended the month 4.28% higher on 23,425.77 and the FTSE AIM recorded a gain of 3.42% in May to close on 821.25. The Euro Stoxx 50 closed the month 2.87% higher on 6,050.54. In Japan, the Nikkei 225 closed May on 66.329.50, gaining 11.88%.

On the foreign exchanges, the euro closed the month at €1.16 against sterling. The US dollar closed at $1.34 against sterling and at $1.15 against the euro.

Gold closed the month trading around $4,578 a troy ounce, a loss of 1.22% in May. Brent Crude closed the month at around $91 per barrel, recording a monthly loss of nearly 17%. Oil prices fell at month end as traders looked for momentum in US-Iran negotiations.

Labour market shows signs of slowing

The UK labour market is showing signs of losing momentum, with rising unemployment, falling vacancies and growing caution among recruiters.

According to ONS, the unemployment rate increased slightly to 5.0% in the three months to March. Job vacancies also declined, falling by around 28,000 to 705,000 between February and April, the lowest level since 2021. In addition, an estimated 100,000 fewer workers were on company payrolls in April, although ONS noted that early payroll data can be subject to higher levels of uncertainty at the start of the tax year.

Survey evidence points to a similar trend. The latest report from KPMG and the Recruitment and Employment Confederation (REC) showed that permanent placements fell at their fastest rate since January, reversing the tentative improvement seen in March. While short-term hiring edged back into growth as businesses sought greater flexibility, overall demand for staff remained weak. Vacancies declined for the 30th consecutive month, although the pace of reduction was the slowest in nearly a year.

Meanwhile, a new report led by former minister Alan Milburn warned that job and career opportunities for young people are shrinking, with one in six expected to be out of work, education or training within five years unless action is taken.

Historic Gulf trade deal set to boost UK economy

A new trade agreement between the UK and the Gulf Cooperation Council (GCC) is expected to deliver a significant boost to the British economy, with Trade Minister Peter Kyle estimating it could generate £3.7bn annually.

This figure is more than double earlier projections, reflecting the broader scope of negotiations, which went further than anticipated on trade liberalisation and services. The agreement covers all six GCC member states – Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE – and was finalised against a backdrop of regional instability and continued disruption to energy and food supply chains.

UK exporters are set to benefit substantially, with 93% of Gulf tariffs on British goods due to be eliminated. Food and drink producers are expected to be among the largest beneficiaries, with products such as cheese, cereals, butter and chocolate gaining tariff-free access. Manufacturers in the automotive, aerospace and electronics sectors are also likely to see new opportunities.

Beyond goods, the agreement maintains existing UK access to Gulf service markets while opening further opportunities for Gulf-based firms. GCC Secretary-General Jasem Mohamed Albudaiwi highlighted coverage across financial services, digital trade, telecommunications and investment protection.

Peter Kyle described the agreement as sending “a clear signal of confidence” to UK businesses navigating an uncertain global environment.

All details are correct at the time of writing (01 June 2026)

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for information only. We cannot assume legal liability for any errors or omissions it might contain. No part of this document may be reproduced in any manner without prior permission.